Instead of doing contribution margin analyses on whole product lines, it is also helpful to find out just how much every unit sold is bringing into the business. For League Recreation’s Product A, a premium baseball, the selling price per unit is $8.00. More importantly, your company’s contribution margin can tell you how much profit potential a product has after accounting for specific costs. The profitability of our company likely benefited from the increased contribution margin per product, as the contribution margin per dollar increased from $0.60 to $0.68.

What is the difference between the contribution margin ratio and contribution margin per unit?

- Contribution margin is the variable expenses plus some part of fixed costs which is covered.

- To calculate the contribution margin, we must deduct the variable cost per unit from the price per unit.

- Gross profit margin is the difference between your sales revenue and the cost of goods sold.

- Regardless of how contribution margin is expressed, it provides critical information for managers.

- For example, in retail, many functions that were previously performed by people are now performed by machines or software, such as the self-checkout counters in stores such as Walmart, Costco, and Lowe’s.

- Thus, CM is the variable expense plus profit which will incur if any activity takes place over and above BEP.

Where C is the contribution margin, R is the total revenue, and V represents variable costs. It represents the incremental money generated for each product/unit sold after deducting the variable portion of the firm’s costs. If the annual volume of Product A is 200,000 units, Product A sales revenue is $1,600,000. The contribution margin can be calculated as an overall number for your company, on an individual product basis, or as a contribution margin ratio metric that divides the contribution margin by revenue to express it as a percentage. In May, 750 of the Blue Jay models were sold as shown on the contribution margin income statement.

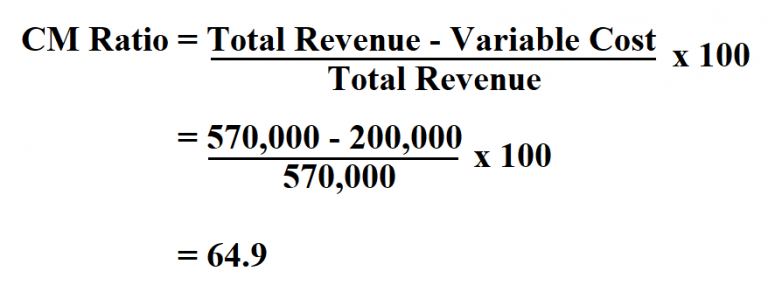

Contribution Margin Ratio:

Still, of course, this is just one of the critical financial metrics you need to master as a business owner. As you can see, contribution margin is an important metric to calculate and keep in mind when determining whether to make or provide a specific product or service. They can use that information to determine whether the company prices its products accurately or is likely to turn a profit without looking at that company’s balance sheet or other financial information.

What is a Contribution Margin and How Do You Calculate It?

A key characteristic of the contribution margin is that it remains fixed on a per unit basis irrespective of the number of units manufactured or sold. On the other hand, the net profit per unit may increase/decrease non-linearly with the number of units sold as it includes the fixed costs. The contribution margin shows how much additional revenue is generated by making each additional unit of a product after the company has reached the breakeven point. In other words, it measures how much money each additional sale “contributes” to the company’s total profits. The contribution margin may also be expressed as a percentage of sales. When the contribution margin is expressed as a percentage of sales, it is called the contribution margin ratio or profit-volume ratio (P/V ratio).

What is the contribution margin ratio formula?

Selling price per unit times number of units sold for Product A equals total product revenue. All you have to do is multiply both the selling price per unit and the variable costs per unit by the number of units you sell, and then subtract the total variable costs from the total selling revenue. Variable costs are not typically reported on general purpose financial statements as a separate category. Thus, you will need to scan the income statement for variable costs and tally the list. Some companies do issue contribution margin income statements that split variable and fixed costs, but this isn’t common. You might wonder why a company would trade variable costs for fixed costs.

Instead, management uses this calculation to help improve internal procedures in the production process. In the United States, similar labor-saving processes have been developed, such as the ability to order groceries or fast food online and have it ready when the customer arrives. Do these labor-saving processes change the cost structure for the company? Based on the contribution margin formula, there are two ways for a company to increase its contribution margins; They can find ways to increase revenues, or they can reduce their variable costs. Contribution margin is the remaining earnings that have not been taken up by variable costs and that can be used to cover fixed costs.

Reduce variable costs by getting better deals on raw materials, packaging, and shipping, finding cheaper materials or alternatives, or reducing labor costs and time by improving efficiency. The concept of contribution margin is applicable at various levels of manufacturing, business segments, and products. Alternatively, the company can also try finding ways to improve revenues. However, this strategy could ultimately backfire, and hurt profits if customers are unwilling to pay the higher price.

The contribution margin per hour of OR time is the hospital revenue generated by a surgical case, less all the hospitalization variable labor and supply costs. Variable costs, such as implants, vary directly with the volume of cases performed. Knowing how to calculate contribution margin allows us to move on to calculating the contribution margin ratio.

On the other hand, the gross margin metric is a profitability measure that is inclusive of all products and services offered by the company. However, the contribution margin facilitates product-level margin analysis on a per-unit basis, contrary to analyzing profitability on a consolidated basis in which all products are grouped together. You can even calculate the contribution margin ratio, which expresses the contribution margin as a percentage of your revenue.

If they exceed the initial relevant range, the fixed costs would increase to $400 for nine to sixteen passengers. For example, in sectors with high fixed costs, such as those with hefty capital investments or sizable research and development expenditures, a higher contribution margin ratio may be needed to achieve viability. This means that, for how to become an independent contractor every dollar of sales, after the costs that were directly related to the sales were subtracted, 34 cents remained to contribute toward paying for the indirect (fixed) costs and later for profit. To cover the company’s fixed cost, this portion of the revenue is available. After all fixed costs have been covered, this provides an operating profit.